Subscribe to Our Insights

Thought Leadership

Is Gold Still in a Bull Market?

By John Hathaway on October 8, 2008

Since the Bear Stearns bailout at the end of the first quarter, the backdrop for gold has unfolded in a more positive way than almost any of its proponents could have imagined. The government takeover of the GSEs, the Lehman Bankruptcy, the disappearance of blue chip investment banks, and continuing intense credit market stress despite the Paulson bailout of the financial system have generated successive new highs in the climate of fear overhanging the financial markets. These successive highs in stress can be measured objectively in the shrinking yields of short dated government securities and escalating credit spreads of all descriptions.

In light of all of this, why hasn’t gold done better? Year over year, gold bullion is up 25.9%, but is well below its peak price above $1000/ounce six months ago. Gold shares have not participated in the flight to safety and have in fact provided disappointing returns over the past six months, during one of the most intense financial market panics of recent history.

Is gold still in a bull market? On the face of it, the question seems absurd. It is tantamount to saying that paper currencies have bottomed out and that the coast is now clear for financial assets. Still, a quick look at gold’s chart shows why the question is pertinent. From viewing this chart, one could argue that when gold traded briefly above $1000/ounce around the timing of the Bear Stearns rescue, it had already fully discounted subsequent, albeit even more dramatic events in the financial markets. At the very least, according to this hypothesis, even though gold might remain in a very long term bull market, for the time being it is not a “good trade”. Asking this question another way, if these horrific financial market developments have been insufficient to drive gold to new highs, what will it take?

As we dissect the internal market developments since the Bear Stearns demise, we can discern (with 20-20 hindsight) a confluence of unusual factors leading to the breakdown in gold’s multi year advance. Our hypothesis is one of mistaken identity. Gold was caught in the cross fire of the unwinding of faux safe haven anti-dollar trades, namely the euro and commodities. The various iterations of anti-U.S. dollar trades leading up to Bear Stearns were undeniably overcrowded. Market Vane sentiment in favor of commodities and the euro and against the dollar were at extreme levels, an accident waiting to happen. On March 17, Market Vane’s bullish consensus was 93 for gold, 73 for copper, 96 for the euro, 82 for light crude oil and 17 for the U.S. dollar index.

The catalyst for a reversal of the anti-dollar trade was news of high level meetings between the U.S., European and Japanese monetary officials to draw up plans to defend the dollar should it crater in response to the Bear Stearns news. These meetings were reported in the press by William Pesek of Bloomberg on August 29, 2008: “Many were equally attentive to how the dollar’s drop was helping to boost oil prices…..The quickest solution is to stop the dollar from falling, a dynamic that might reverse the increase in oil prices.” It would not be surprising if word of these discussions was disseminated to selected financial institutions and their clients well before the press coverage of a dollar defense strategy, originally reported by of Nikkei News.

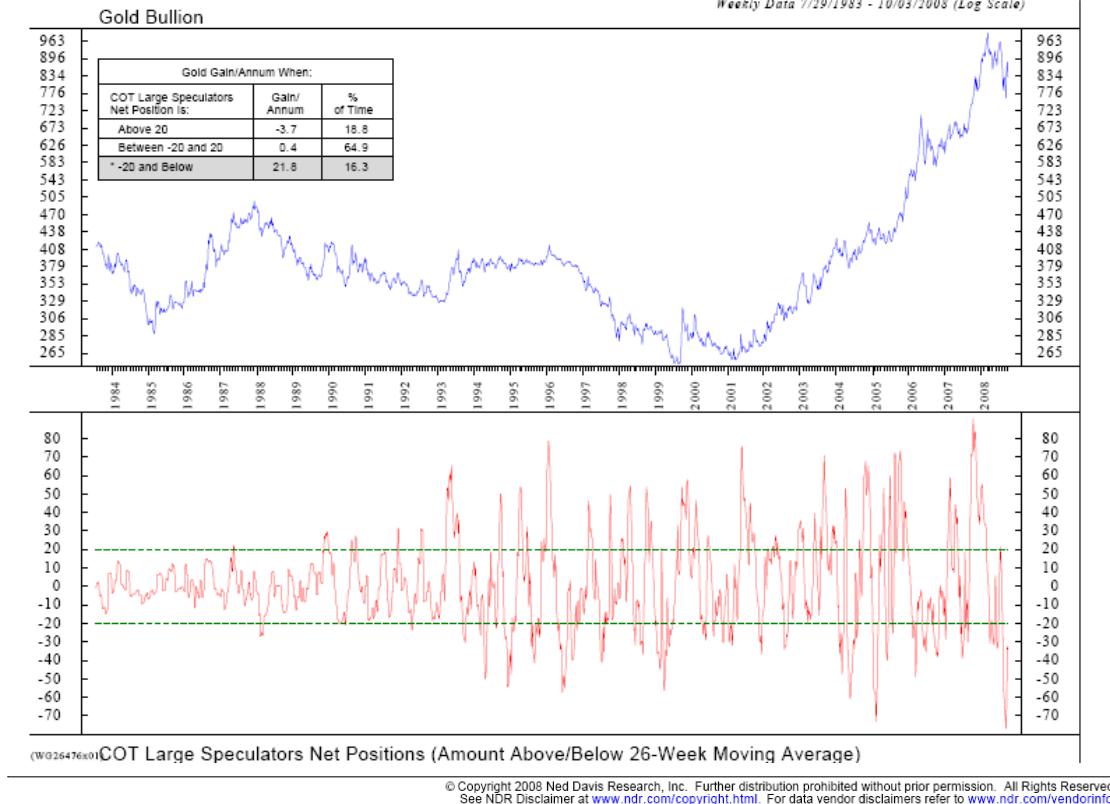

The prospect of a possible line in the sand translated into a brick wall for the euro. The exchange rate has declined from 1.60 to 1.35 or 15.6% in the space of a few months. Unwinding of the long euro-short $US began in earnest in mid July ’08 and reached panic proportions by early September. Related trades including commodities and especially oil were also collapsed. Covering dollar shorts created the illusion of a strong dollar. Given the tight correlation in recent years between the euro and gold, long gold positions held by hedge funds were dumped. The swings in Comex positions depicted by the Ned Davis chart are consistent with interpretation of a panic liquidation. The one month swing from July to August for gold was the fifth largest four week drop in net speculative positions over the last twenty-five years.

Comex futures are paper contracts typically settled for cash. Little physical gold changes hands. For example, Tocqueville holds nearly 100,000 ounces of physical gold at a Comex warehouse. While our gold is counted as part of the underlying physical metal to support the trading of paper contracts on Comex, it is not for sale and cannot be hypothecated. During the recent meltdown, bullion dealers inquired whether Tocqueville wished to sell its gold to take advantage of record premiums for converting Comex good delivery bars into coins. The U.S., Austrian, and South African mints report that they have had to ration or suspend sales of gold coins due to shortages of metal. Accounts of shortages in physical gold trading centers are numerous: “Wealthy Investors Hoard Bullion (Financial Times 9/30/08).” Jeremy Charles, chairman of the London Bullion Market Association, is quoted in the article as saying “There is an enormous pick-up in investment demand. I have never seen a market like this in my 33 year career.” To add to the conundrum, physical holdings of gold ETFs have climbed to all time record levels.

Over the past few months, the price of gold has not been set by the physical markets, however. It is set on the Comex platform where gold can be shorted naked. Unlike the process of shorting a stock, requiring a borrow prior to the execution of a short sale, funds trading on the Comex can short paper contracts that typically settle in cash and do not require possession of physical gold. According to one bullion trader we spoke with recently, there is only very light volume trading at the London fixes, where physical metal changes hands. All of the action has been on the Comex, and even there the volumes are light. Most of the recent trading appears to be linked to movements in the euro by relatively small players in a thin market.

It seems that the likely source of the glut of paper gold was momentum driven hedge funds that had been massively wrong footed in an overcrowded trade. The 2008 summer gold panic was a liquidation of paper that never translated into the physical deliveries to satisfy record demand. At the end of the day, the paper shorts represented by hedge funds, banks and their clients fell into a bear trap of their own making. There was no physical with which to cover. This explains the unprecedented 17% short covering rally in the space of only two days (September 17 and 18). The only similar episode in recent memory was the short covering rally in 1999 triggered by the Central Bank agreement to limit gold sales. Chart patterns back then were less favorable than today. At the very least, it is premature to declare an end to the bull market in gold and the bear market in paper. It is more likely that this massive shakeout has set the stage for a dynamic advance.

What will drive a further advance in gold? Let’s start with the implausible assumption that the worst of the credit crunch had been already discounted when gold scaled $1000. Let’s also assume, an even greater stretch, that the Paulson bailout succeeds in restarting the wheels of lending and commerce. Finally, let’s toss in an end to the decline of asset prices and the commencement of a bull market in equities. The unequivocal precondition for these felicitous events would be the transformation of the dollar and other paper currencies as we know them. The socialization of credit in the U.S. may well work the miracles as its proponents claim, but not without stiff costs. We suspect that two inescapable costs will be inflation and negative real interest rates as far as the eye can see. Both of these outcomes are friendly to gold. Neither is likely to improve the credit rating of the dollar or increase the desire of non U.S. investors to increase their holdings of U.S. Treasuries.

We believe that a future downgrade of U.S. sovereign credit is a strong possibility. It would defrock U.S. Treasuries of their safe haven status. In the late 1970’s, they were dubbed “certificates of confiscation”. We fully believe they will once again be referred to in a similar manner as a direct result of current and still to come interventions by the government to shore up financial markets. On September 16, 2008, The People’s Daily, which is the official newspaper of the Chinese Communist Party, commented: “The world urgently needs to create a diversified currency and financial system and fair and just financial order that is not dependent on the United States.” There is similar commentary from other major foreign investors in U.S. Treasuries.

The experience of the past six months has unmasked other faux safe havens. Paramount among these are the euro and economically sensitive commodities such as base metals and oil. While we view the euro as perfectly capable of rallying to new highs versus the dollar in the coming months, we believe it is even more likely to disintegrate than the U.S. dollar. A euro permanently above 1.60 would be catastrophic for euro land and would be politically intolerable. Finally, we note that there is nothing automatic regarding the correlation between the euro and the U.S. dollar gold price. The last period of prolonged dollar strength versus the euro coincided with strength in both the dollar and euro gold price.

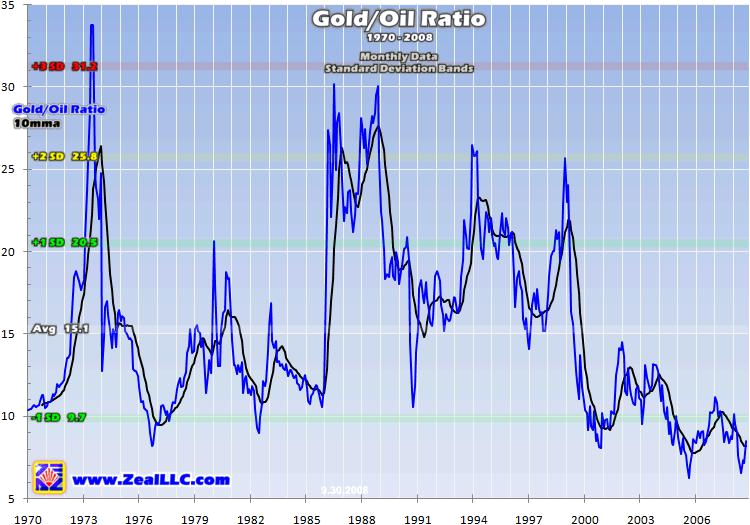

Economically sensitive commodities have multiple shortcomings as safe havens against economic turmoil. First, economic turmoil undermines demand for them. Second, rising prices in real and even in nominal terms are economically disruptive and, by the way, cause economic turmoil. Third, they are impossible for most investors to take physical possession of. As the chart below shows, gold is cheap relative to oil. There is no rule that states that gold must revert to a more normalized relationship. However, gold trending higher against oil would signify that investors had rediscovered its monetary traits and are in the process of revaluing the metal versus economically sensitive commodities.

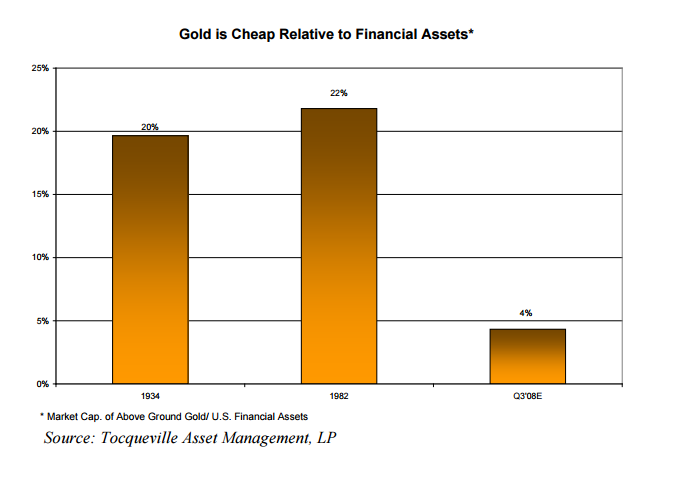

The remaining “safe haven” to be unmasked is U.S. Treasuries which sport yields significantly below nominal rates of inflation. For now, safety seeking investors prefer to lose money slowly in Treasuries than in supposedly riskier assets. Should the bailout and whatever other extreme measures the government undertakes meet with success, the safety of Treasuries will be exposed as were the euro and economically sensitive commodities as investors rush for the exits. We believe there is pain ahead for those hiding in Treasuries. As the table below shows, gold is cheap relative to financial assets and that there is plenty of room for gold to be reassessed even in a more favorable economic climate.

As the table below shows, there is a paucity of physical gold to receive capital flows from failed safe havens. The magnitude of the upside potential is expressed rather eloquently in the proposition that the estimated float of physical gold (45,000 – 50,000 tonnes) is roughly equal to the buying that would be generated by a mere trickle of slightly more than 1% of global pension fund assets in its favor. In our view, gold trading steadily at $2500 is not unthinkable. Gold at $2500 would not be economically disruptive but result instead from disruption itself. Until trust is restored in the mechanisms and instruments of government, namely paper money and, more recently, large swaths of the financial system, we like the metal’s chances to reside comfortably in four digit territory. We believe that gold mining shares, which have provided very disappointing returns over the past six months, are due for a significant revaluation once investors view the $1000/ounce threshold as a floor rather than a ceiling.

The answer as to whether or not gold remains in a bull market should not overly depend on the pessimism currently rampant in the financial markets. While worst case outcomes may still be in the cards, as contrarians, we suspect they are close to being fully priced into the mix, at least for the time being. A better test for investing in gold is on what basis a case can be made in a more favorable climate for financial markets. That scenario might include declining risk spread, a bottom in housing, and some hope for resolution of the credit crisis. The linkage of gold to the euro is a temporary fact of life. We fully expect both the dollar and the euro to lose value against gold. From time to time they will take turns leading the race to the bottom but we have little doubt the gold price expressed in either currency will be significantly higher within a reasonable time frame. In our view, nothing could be better for gold than for European investors to lose faith in the euro in the same way that investors have lost faith in the dollar, the financial system and financial assets in general. If dollar strength against the euro restores some semblance of stability to the financial scene, as ludicrous as the thought might be, gold is not automatically the loser.

Long lines of investors buying physical gold, even though they may not have affected the price near term, signify a widespread loss of trust. In our article “The Investment Case for Gold” written 1/22/02, we described three factors that would drive the gold price to all time highs: supply and demand, macroeconomic, and metaphysical. Of these three, the most important is metaphysical because it represents a shift in widespread social and institutional belief structures and thought patterns. The events of the past six months have all but destroyed faith in the competence of political leadership, government and financial institutions and the expectation that expert financial professionals can produce satisfactory returns. Gone too is the belief that housing prices will rise forever and that taking on debt is a good idea.

The bleak climate of opinion that has settled in will not easily be whisked away by new government policies. It will not be dislodged by cheery reports on CNBC, a positive set of government statistics, or encouragement from bullish gurus. A preference for risk avoidance is here to stay for quite a while, even after the markets find their ultimate lows. This was the case in the 1970’s following the bear market bottom in December, 1974. Cultural lag is a powerful force and can influence behavior long after the worst has been seen. Once expectations and beliefs become imbedded and are reinforced by experience, the swing of pendulum back towards a full appetite for risk taking might take half a generation. For this reason, we expect the price of gold to continue its rise against all paper currencies for several years to come.

Given gold’s disappointing behavior thus far as the credit crisis unfolds, it is understandable why so many investors appear to remain on the sidelines. The bull market in gold is intact. The dynamics of the ongoing financial crisis can be summed up in the escalating tension between inflation and deflation. The market-induced deflation of asset values and income streams comes at a time when debt relative to GDP is at all time highs. The options for government policy are

stark: either let the burden of debts further crush economic activity, or crank up the printing presses to devalue paper currencies so as to relieve debt burdens. The question for anyone on the sidelines contemplating gold is whether it is possible or necessary to time perfectly a strategic commitment to the one asset class that will survive and most likely benefit under either outcome.

John Hathaway

Portfolio Manager and Senior Managing Director

© Tocqueville Asset Management L.P.

October 8, 20

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

Mutual Funds

You are about to leave the Private Wealth Management section of the website. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the Tocqueville Trust Mutual Funds. Please consider the investment objectives, risks, and charges and expenses of any Mutual Fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Mutual Fund section of the website, by contacting an authorized broker/dealer, or by calling 1-800-697-3863.Please read the prospectus carefully before you invest. By accepting you will be leaving the Private Wealth Management section of the website.