Subscribe to Our Insights

Thought Leadership

Monetary Tectonics

By John Hathaway on November 24, 2014

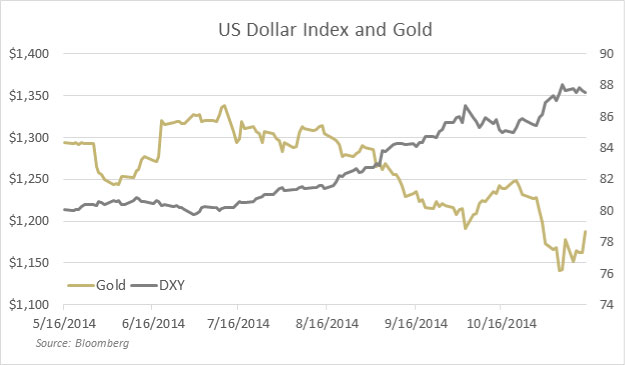

The “strength” in the dollar appears to have been the proximate cause of the recent selloff in gold. The rise in the dollar index (DXY) is taken by most to mean that the dollar is actually strong. The chart below shows the inverse correlation between the DXY and the dollar gold price. This discussion will examine the very meaningful difference between the dollar’s relative and absolute strength, and look at the widening fissures beneath the façade of strength – fissures that, as yet, appear to have had little impact upon the investment consensus.

The DXY index is not the dollar; it is a measure of the dollar’s relative strength. The principal components of the DXY index are the Euro (57.6 percent) and the Japanese Yen (13.6 percent). The balance (28.8 percent) consists of the Canadian dollar, British pound, Swedish krona, and Swiss franc. Therefore, the DXY index says absolutely nothing about the inherent virtues of the US currency. Instead, it reflects capital flight from yen- and euro-denominated assets from regions where the respective central banks have hatched well documented schemes to devalue those currencies as the antidote to economic weakness. There are many reasons why the dollar may remain strong against the core components of the DXY. However, whatever virtues others may see in the DXY’s ascendant pattern, we see the potential for monetary chaos.

The DXY is mute on the matter of the rapidly waning usage of the US currency to settle international trade. Deals to bypass the greenback seem to proliferate daily. The dollar has become an impediment to trade for even our closest and most important trading partners. Canada has just announced a series of deals to trade directly in renminbi, following similar actions by several Latin American countries. The Wall Street Journal (11/14/14) reports that Russia will “receive renminbi as payment for a significant flow of oil” to China. Vladimir Putin commented, “we’re moving away from the diktat of the market that denominates all commercial oil flows in US dollars.” As mentioned in our third-quarter investor letter, first-half trade cleared in renminbi totaled $18.3 billion, double the previous year. The institutional plumbing to circumvent the dollar is being put into place. Examples include the launch of the Shanghai Gold Exchange in September of this year, as well as the formation of the BRICs bank (in the second quarter), on the model of the World Bank, to facilitate non-dollar transactions.

In addition, Russia has announced that it is developing its own version of SWIFT, a network that enables financial institutions to communicate electronically in a secure fashion, which it expects to launch in 2015. The clear intent is to bypass Western financial institutions and conventions.

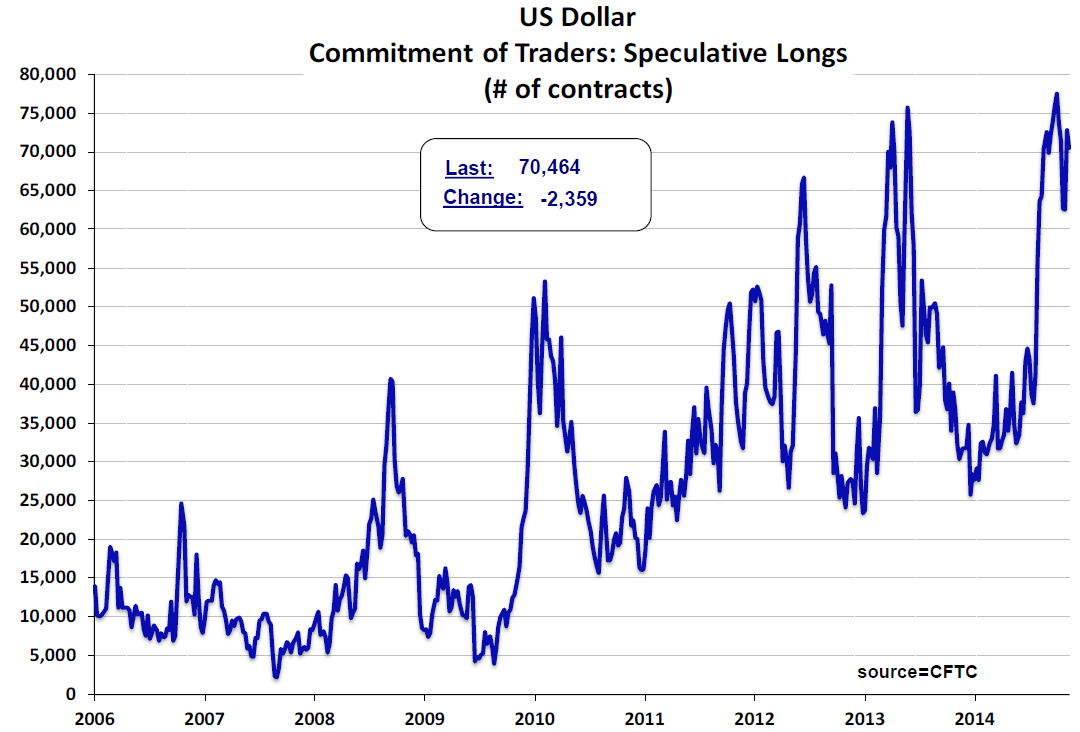

In our opinion, a world in which the dollar becomes increasingly marginalized as a reserve currency will look substantially different. As noted by Andrew Smithers in the Financial Times (11/12/14), the US is a massive hedge fund, “long equities and short debt,” with an international net debtor position equivalent to 31 percent of GDP. As long as dollar reserves have utility, dollar-denominated assets can thrive. Utility is in large part a matter of perception and confidence, in our view, and the fundamentals underlying the notion of a strong dollar are sliding in the wrong direction. At the moment the long dollar trade seems extremely crowded, with CFTC speculative long exposure near record highs (see chart below). In the short term the dollar may seem to be a lifeboat for unwanted yen and euros, but in the intermediate to longer term it is a lifeboat that suffers from the flaws inherent in all paper currencies. Today’s clamor for dollars will, in our opinion, become tomorrow’s dollar overhang.

Source: MeridianMacro

One of the fundamentals in the equation for a strong dollar is a perception of US economic strength. We believe that capital flight explains popular stock market averages at all-time highs. Early warning signals of a possible global downturn include a numerous array of disappointing reports on the US economy, the third quarter GDP contraction in Japan, commodity prices breaking down to new lows (including copper, the most prescient of all), and the continuing widening of the gold/silver ratio. Beggar-thy-neighbor competitive devaluations in the 1930s prolonged the depression. It is hard to see why similar actions in Europe and Asia will not have a similar impact. Persistent and extensive euro and yen weakness relative to the dollar, which would translate into a further rise in the DXY, would most likely undermine the US economy and pressure the Fed to resume quantitative easing.

It appears to us that the recent few months in the financial markets represent a victory lap of sorts for financial assets, a celebration of the so-called end of quantitative easing, and perhaps a high-water mark for confidence in the Fed. What better way to punctuate this success than for gold to print at a 4½ year low? A headline-making low in the gold price, in tandem with popular stock market averages at all-time highs, is simpatico and harmonious for policy makers, the financial media, and most investors.

Selling gold, synthesized by bullion bankers, turns out to be as easy as creating dollars out of thin air as practiced by central bankers. The prices quoted on Bloomberg, CNBC, et al. are putatively for gold, but no physical gold is involved. Most of those selling gold do not have it in the first place. As with a bookmaking operation, the only things that change hands are credit instruments, in this case referenced to a gold benchmark such as the London fix or Comex close. Cash or credit – not gold bars – is used to settle. It is a gold trade in name but not in substance.

The gold price, then, is an exchange rate. The dollar price of gold is similar to the dollar price of euros or yen; and as it turns out, it is just as easily manipulated. Revelations of fines levied against major banks for FX (currency-exchange market) transgressions, including prominent bullion banks, are just beginning to spill into the headlines. Regulatory settlements totaling $4.3 billion were announced on November 12th with the UK, the US (CFTC and OCC), and the Swiss. The banks involved include Citigroup, UBS, JP Morgan, HSBC, and RBS. As one observer notes, this is just the first step in a long litigation road for the sector. The Fed and German regulators have yet to weigh in. A more widespread connection to gold-price manipulation is not distant, as Swiss regulators have already charged misconduct by UBS precious-metals traders (click here).

The weakness of gold relative to the dollar and financial assets can be seen as an expression of the investment and policy-making consensus. It rests, it would seem, upon a delusional faith in the miraculous power of money-printing. A new generation of central bankers has transformed the staid portfolios of their predecessors – consisting of inactive pools of currency reserves and bullion – into hedge funds that trade derivatives, futures contracts, and instruments too exotic to comprehend. The Chicago Mercantile Exchange invites them to do so. In Exhibit 1 of a January 29th letter to the CFTC (click here), the CME group offered special discounts to central banks “outside of the United States” to trade such un-central-bank items as stock index futures, foreign exchange, agricultural commodities, energy, and of course precious metals. It would appear that the CME has become an important interchange by which central bankers can tweak the financial markets to affect the thought process and behavior of the investor.

When it comes to tweaking, the Swiss National Bank gets first prize. As of August 2014, the SNB balance sheet totaled CHF 522.3 billion, or 1.4 times Swiss GDP. The asset breakdown is 74 percent government bonds (the bank is one of the top five holders of US Treasuries), 11 percent other bonds, and 15 percent equities. The policy goal of the Swiss strain of monetary insanity is to peg (cheapen) their currency to 1.20 euros, override free-market capital flows that would be resolved in a stronger exchange rate, and thereby boost the Swiss economy. Note the 15-percent equity position in the SNB composition of assets. In its fight to maintain the peg, the SNB conjures up Swiss francs out of thin air, with which it buys euros. It then converts some of the euros into US dollars and buys US stocks, most likely on the CME. And there you have tweaking extraordinaire: Local currency created on a computer pushes up the value of the US dollar and US stock indices to benefit the Swiss economy.

Grass-roots opposition to this policy of currency debasement has taken the form of a referendum (to be held November 30th) that would require the SNB to increase substantially its holdings of gold. Win or lose, the referendum reflects the stirring of popular resistance to central-bank-induced financial repression. In our opinion, monetary unrest will not be contained within the Swiss frontier.

The modern-day central banker trades with counterparties that are giant commercial banks with derivative books of disturbing scale and complexity. It seems impossible that these commercial exposures could be constructed and maintained without the knowledge and complicity of the official sector. For example, Deutsche Bank, already a defendant in 1000 lawsuits, claims derivative exposure that is 20 times the GDP of Germany and 5 times that of the entire Eurozone. It is not a great leap to suggest that central-bank traders and their megabank opposites – spawn of the same gene pool, schooled in the same institutions, career paths intertwined, frequenters of the same conferences, and just a speed-dial away – are ideologically indistinguishable and intellectually and morally corrupt in equal proportion. We applaud the efforts of litigators and plaintiffs already in process and those in the wings, and look forward to the depositions and discoveries yet to come.

Whether the eventual cessation of manipulative practices translates into a change of trend for the gold price remains to be seen, although it seems logical that the bullish consensus for financial assets equates to a complacent and very large short position in gold that will have to be covered (37.5 million troy ounces). More important, as we demonstrated in “Let’s Get Physical”, there is a massive asymmetry between paper claims on gold and physical metal. Should Western investment demand, accustomed to acting only through financial instruments such as ETF’s, futures contracts, and derivatives, revive only modestly, the fragile link between paper claims and the real thing – which has been stretched and contorted by extreme rehypothecation (the use by financial institutions of clients’ assets, posted as collateral) – could easily shatter. The major winners in a systemic repricing of gold will be those who own or produce the real thing.

In his recent investor letter “Faking It,” Paul Singer of Elliott Management attacked the rampant falseness of current-day capital markets: “Nobody can predict how long governments can get away with fake growth, fake money, fake financial stability, fake jobs, fake inflation numbers and fake income growth. Our feeling is that confidence, especially when it is unjustified, is quite a thin veneer. When confidence is lost, that loss can be severe, sudden and simultaneous across a number of markets and sectors.”

Since 2008 global debt has grown by 40 percent, a far greater pace than global GDP. There has been no deleveraging on a global basis. The just-published report on the global economy by the International Centre for Monetary and Banking Studies warns of a “poisonous combination of high and rising debt and slowing nominal GDP.” The global debt-to-GDP ratio was 215 percent in 2013 vs. 200 percent in 2009. In our opinion, the expectation for anything beyond anemic growth is a fantasy: Debt-service burdens, even at zero interest rates, will not allow for more. Unfortunately, only the achievement of sustained robust growth will restore the possibility of servicing debt at normalized interest rates. We believe that radical monetary policies are here to stay, even if the baton of debasement is passed from one central bank to another.

Swelling distrust of, and disrespect for, the dollar’s reserve-currency status is becoming another headwind. To us, these developments suggest that the tectonic plates of monetary conventions are beginning to shift in a way that will lead to a significant revaluation of gold. A critical state will be reached when markets and policy makers realize that additional credit creation does not stimulate growth.

Until monetary sanity is restored, it seems to us that that the world of investment will remain a hall of mirrors. What is real and what is illusion? The blur between the two can only result in distortion and miscalculation for all markets. The paper-money prices of gold, oil, labor, capital, and all other factors of production are real enough in the moment. The problem is that understanding the forces that cause them to be one number or another, now or in the future, is made exceptionally challenging by the tinkering of central banks. Without real money, the risk-free rate of return (the rate on short-term US government bonds) – the standard by which all investments, liquid or illiquid, are gauged – is either indeterminable or non-existent. In the long run, little good can come from its absence.

The investment rationale for gold is the inverse of that for all paper currencies. Cheering for the rise in the dollar relative to other currencies, as measured by the DXY, is in our opinion seriously misplaced. The rise in the index is more a matter of sinking non-dollar currencies (or, more precisely, systemic subsidence) than an ascending dollar. No paper currency offers protection from monetary transgressions because of national borders: What happens in Europe, Japan, or China does not stay in Europe, Japan, or China. To function well, the global financial system must be seamless.

In the absence of robust global growth, debasement of the euro and the yen will ultimately force devaluation of the dollar – but against what? When no paper currency is left standing from multiple rounds of competitive devaluation, there will be no choice other than to reconfigure global financial arrangements. We believe that gold, revalued in a very substantial way, will be integral to the process of reconfiguration.

John Hathaway

Senior Portfolio Manager

© Tocqueville Asset Management L.P.

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

Source: Tocqueville

Author: John Hathaway

Mutual Funds

You are about to leave the Private Wealth Management section of the website. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the Tocqueville Trust Mutual Funds. Please consider the investment objectives, risks, and charges and expenses of any Mutual Fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Mutual Fund section of the website, by contacting an authorized broker/dealer, or by calling 1-800-697-3863.Please read the prospectus carefully before you invest. By accepting you will be leaving the Private Wealth Management section of the website.