Executive Summary:

“It was the best of times. It was the worst of times.” That quote from Charles Dickens’ novel A Tale of Two Cities seems to capture the events of 2020. Themes from the Dicken’s novel ‐ ‐ duality, revolution and even insurrection ‐ ‐ have all come into play for investors over the past year. At the beginning of 2020, most investors were focused on the strengths of the economy in terms of record low unemployment, rising wages, recently completed trade deals with China and Mexico, low interest rates and reduction in business regulation. No one did or could have foreseen the disruption of the COVID virus that was coming. Investors and the population at large continued basking in the longest economic expansion on record and the stage seemed to be set for moderate growth, stable markets and the presumptive reelection of President Trump. Indeed, if there is an economics lesson from the pre‐COVID period, it is that the U.S. economy can run hotter with a stronger job market and larger fiscal deficits than previously believed without incurring starkly rising interest rates and inflation. Of course, then in late February and early March, everything changed, but those lessons will likely have important implications for the Biden administration. (see figure 1)

(Figure 1)

(Figure 1)

The year global equity markets just experienced marked near historic volatility and was characterized by geographic, socioeconomic and sectoral disparities (see figure 2). Considering the speed and severity with which markets reacted to the outbreak of COVID‐19, and the initial restrictive actions of governments and private individuals and businesses, and then the gradual and arbitrary reopening and recovery, marred by fits and starts, it does seem somewhat remarkable that markets achieved a positive result at all, much less one that put all of the major indices at or near record levels.

(Figure 2)

(Figure 2)

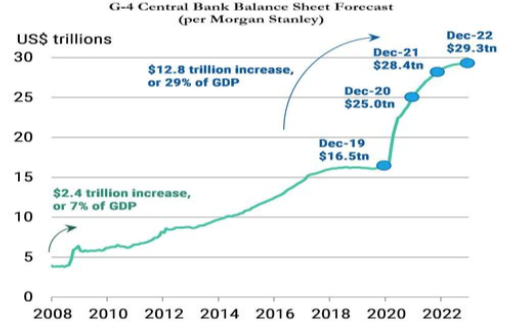

The main reason for the strong rally from March lows in global stock markets is the prompt and massive reaction of the world’s central banks which, by year’s end, had pumped into their financial systems nearly $30 trillion dollars and seemed intent to go for more as we look toward the new year. This comprehensive intervention is orders of magnitude larger than the similar actions taken during the Great Financial Crisis in 2009. Moreover, they were accompanied by significant fiscal responses from the major governments unlike what occurred in the previous global crisis. Indeed, the sum of the Fed and ECB balance sheets are up more than 70% compared with last year (see figure 3).

(Figure 3)

(Figure 3)

All this liquidity inflated global equities and other assets, but with varying results. Some of that disparity was due to the different measures taken by of governments to contain the pandemic. The U.S. markets did well as represented by the S&P 500 and better than most European markets. Arguably the U.S. public and private sector authorities took a relatively more pragmatic approach regarding the trade‐offs between public health with the needs of the economy. Interestingly, the dollar lost more than 8% against the Euro during the earlier period where the Europeans seemed to prioritize the health

aspect above economic concerns. However, some Asian equity markets did even better, having experienced the pandemic earlier.

Commodities, aside from oil, also benefitted from the liquidity and outperformed U.S. equities as the dollar weakened considerably (see figure 4).

(Figure 4)

(Figure 4)

Looking toward 2021 and beyond, questions linger about the longer‐term impact of the pandemic and the consequences of massive monetary and fiscal intervention might have on markets, the economy and important macroeconomic variables such as interest and currency exchange rates, financial assets, commodities. As important, perhaps, or even more so, what will be the impact on politics?

For most market commentators, the emerging consensus view is continued optimism for the economy and for equities, concerns about fixed income assets due to the expected rise in inflation and a concomitant rise in yields, doubts about the strength of the dollar and therefore rising raw materials and precious metals pricing.

This consensus contains some inherent contradictions that merit a second look.

The first is that the sharp market rallies have already discounted a strengthening global economy.

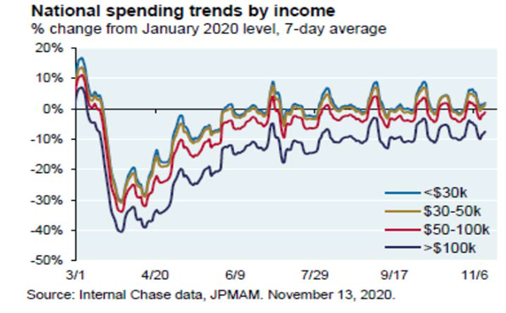

Second, recovery in post pandemic consumption could disappoint. Most consumers have already returned to pre‐pandemic levels of spending. The composition of spending may have changes, but the level is such that there is little room for mean reversion in middle and lower income level consumer spending (see figure 5).

(Figure 5)

(Figure 5)

Only the higher income brackets are still below where they were pre‐pandemic spending levels. If spending by high income individuals recovers more it may be in categories such as travel, restaurants, and luxury goods. But upper income brackets are the ones that will be hardest hit by Biden Administration likely tax increases, so the effect may be muted.

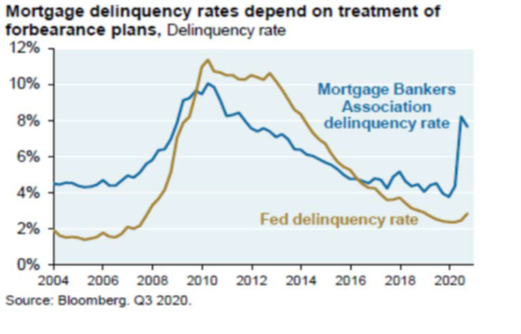

The underlying health of the consumer economy is also misleading because there is a great deal of legally mandated mortgage and rental forbearance (see figure 6). Depending on how banks and landlords treat deferred and foregone payments will affect how quickly consumers can expand their discretionary spending.

(Figure 6)

(Figure 6)

Also, while the scientific community has proven remarkably successful in developing vaccines to address the pandemic, the disjointed and underfunded approach to distributing the vaccines has been disappointing. Nor is there any certainty over how long the vaccine will last. Thus, optimism over the vaccine could be overdone or premature.

Finally, some observers believe that the rally has left U.S. equities overextended from a valuation standpoint. Across many metrics the current valuation of the U.S. markets is high. In prior cycles when those thresholds were reached market performance has lagged.

For all these reasons, we are wary of becoming too enamored of the prevailing consensus and continue to stress our value discipline in stock selection.

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized. References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

You are about to leave the site of Tocqueville Asset Management, L.P. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the any mutual fund managed by Tocqueville Asset Management, L.P. Please consider the investment objectives, risks, and charges and expenses of any mutual fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Poplar Forest (www.poplarforestfunds.com), by contacting an authorized broker/dealer, or by calling 1-877-522-8860. Please read the prospectus carefully before you invest. By accepting you will be leaving the site of Tocqueville Asset Management, L.P

You are about to leave the site of Tocqueville Asset Management, L.P. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the any mutual fund managed by Tocqueville Asset Management, L.P. Please consider the investment objectives, risks, and charges and expenses of any mutual fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Tocqueville Funds website (www.tocquevillefunds.com), by contacting an authorized broker/dealer, or by calling 1-800-697-3863. Please read the prospectus carefully before you invest. By accepting you will be leaving the site of Tocqueville Asset Management, L.P