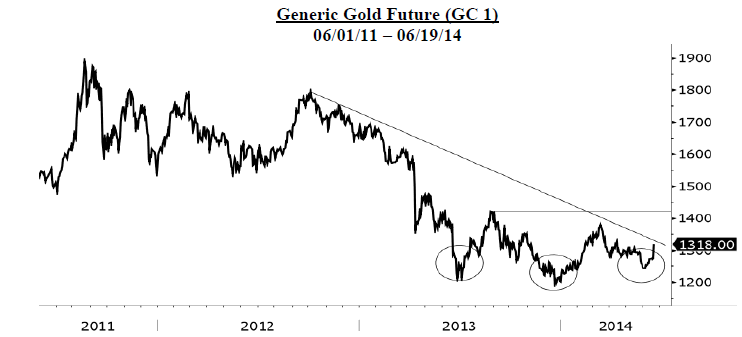

The precious metals complex, both mining shares and bullion, appears to be in the process of completing a major bottom extending back to mid-2013. The chart below depicts this action quite clearly in the form of what technical analysts refer to as a reverse or upside down head and shoulder pattern, a classic indication of a possible trend reversal. While further upside is required for conclusive evidence, and more testing is quite possible over the summer, we are becoming more comfortable with the proposition that the downside potential has been fully exhausted after nearly three years of declining prices and that the stage has been set for a major advance in the years to come.

Source: International Strategy & Investment Group LLC

Many other components of a major bottom appear to be lining up as well. Sentiment gauges are constructive, meaning that most investors remain negative, disinterested, or off balance. Please refer to the chart from Ned Davis Research (below) as well as the array of sentiment indicators appended to this letter.

Source: Ned Davis Research

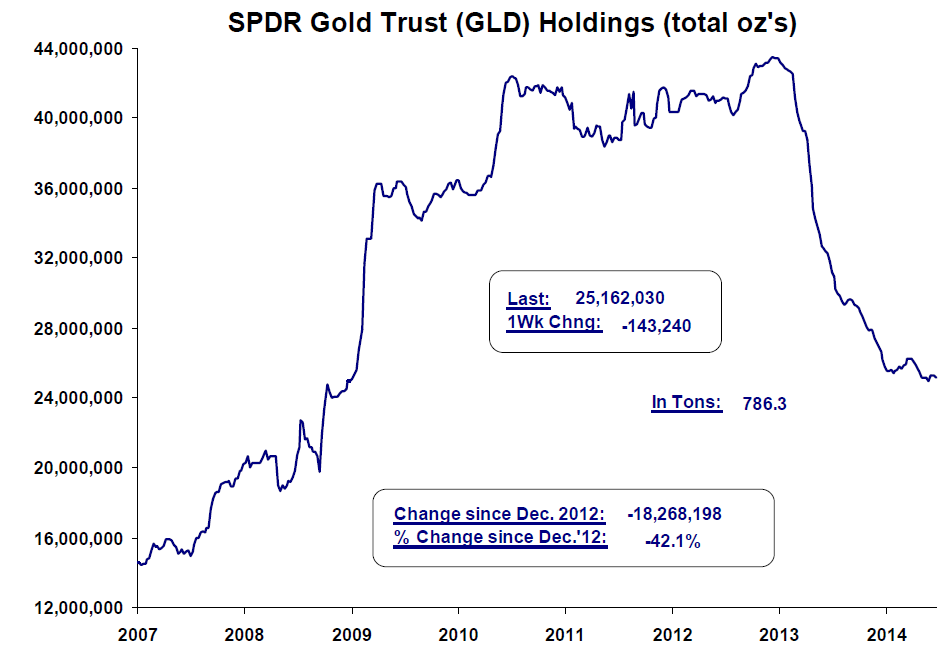

Money flows, using GLD assets under management as a proxy, are beginning to show signs of stabilization, if somewhat tentative.

Source: MeridianMacro

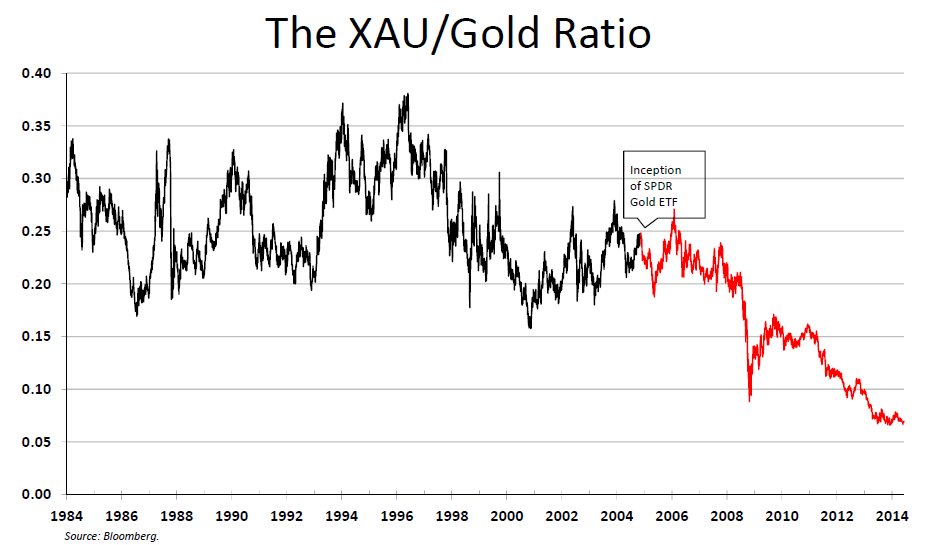

Valuations of precious metals mining shares, both gold and silver, continue to creep along at what we consider to be rock bottom levels. Fundamentals are improving. Earnings and cash flow are beginning to rise due to higher bullion prices and radical cutbacks in costs and capital expenditures.

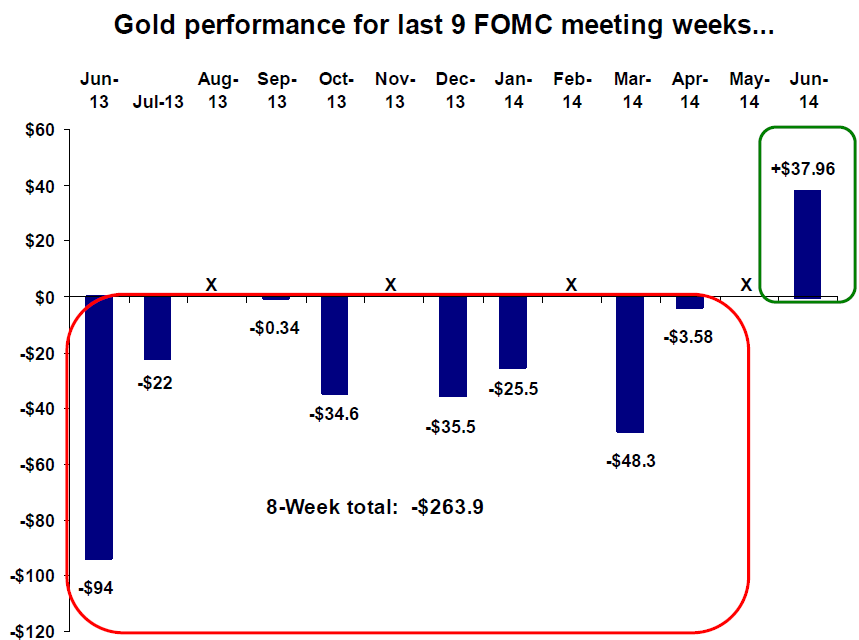

News headlines, particularly FOMC pronouncements which have had a particularly negative effect on price behavior, appear to have lost their sting. It appears that the perception of Fed tapering, which has for the past few years represented short hand for investor comfort with the course of monetary policy, is at worst old news fully digested by precious metals markets, and at best (from a gold investor’s point of view) becoming problematic.

Source: MeridianMacro

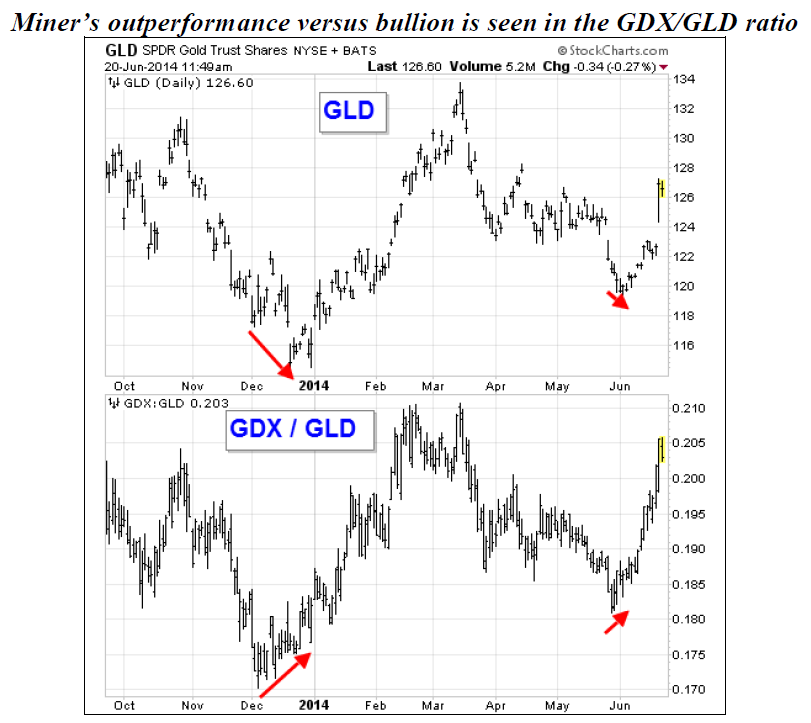

Another positive sign is that the mining shares seem to be leading metals prices. This sort of price behavior has been associated with advancing stages and just the opposite of the period in 2011 when precious metals shares began to underperform advancing bullion prices.

Source: ChartWorks

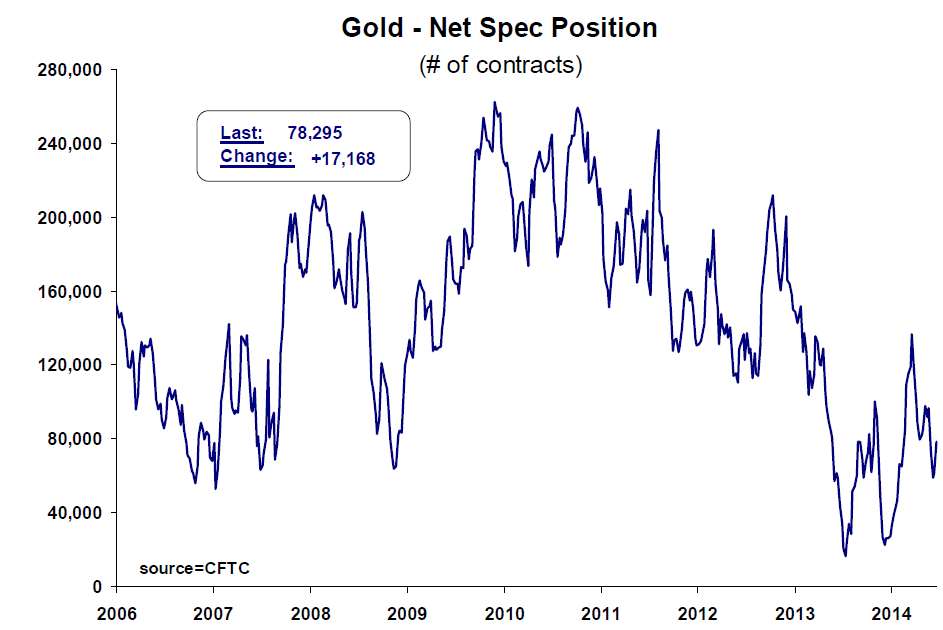

The position of the market remains extremely short. There is plenty of upside potential based on speculative Comex positions swinging from short to long exposure.

Source: MeridianMacro

It is interesting that the below chart of yields on the ten year treasury showing a head and shoulders top is almost a mirror image of the first chart showing a reverse head and shoulders formation for gold. With CPI inflation numbers beginning to rise, the implications of this particular chart might seem counterintuitive. One possible explanation would be that plunging yields would signify coming economic weakness that could in turn cause a U-turn in the Fed taper:

Source: International Strategy & Investment Group LLC

Finally, a chart of the trade weighted dollar index shows persistent weakness despite the market consensus for economic growth during the remainder of 2014. This is also counterintuitive because the dollar would normally show strength during periods of robust economic growth. Rallies from these levels have been progressively weaker, and so this needs to be watched carefully. A breakdown from here could result from the onset of unexpected economic weakness or, another possibility, backlash from the “weaponization” of finance in the form of sanctions and fines levied against foreign entities:

Source: International Strategy & Investment Group LLC

Regardless of the many cross currents suggested by some of the foregoing observations, the current position of the market seems quite similar to 1998-1999 when the 20 year bear market in gold concluded: gold was a joke, investor exuberance in stocks was unprecedented, and the investment consensus was for endless fair weather. For those seeking an uncorrelated asset to protect wealth accumulated in the bull market of the past four years, we respectfully suggest getting reacquainted with this pariah.

The fundamental rationale for exposure to gold remains in our opinion rock solid and unchanged from five years ago: radical monetary policies will lead to debasement of paper currencies and in so doing will undermine wealth that is wrapped in financial assets. This has not been a profitable or popular view since August of 2011 when gold peaked at $1900/oz. Central bank balance sheet expansion and money printing has not caused the sort of inflation that would prove troublesome to the financial markets. In fact, just the opposite has occurred. Money printing has pumped up financial asset values to extreme and most likely dangerous levels, while cost of living inflation has remained muted. The bull market in equities and bonds has been a major headwind for precious metals.

Compared to 2008, global financial leverage has increased 40% to $100 trillion. This record leverage is manageable only because interest rates are historically low. Extreme high valuations of financial assets are supported by DCF models based on ultra-low interest rates. Higher interest rates will (1) undermine fundamentals, making record debt levels more problematic, and (2) deflate valuations of the anticipated future cash flow generated by equities, junk bonds, and sovereign debt.

The catalysts for a dynamic upward shift in the direction of precious metals are numerous but the timing remains elusive. If the bull case for gold were to be widely articulated, the upside potential would not be compelling. If the timing were clear, it would be uncharacteristic of the start of a prolonged advance in any market.

The many catalysts that could drive gold higher are precisely those that the market consensus does not expect, wish for, explain away, or simply ignores. These include but are not limited to problematic inflation, a potential bear market in financial assets, economic stagnation or decline, a lengthy period of rising interest rates, continued flow of bad news on the geopolitical front, the stealthy resurgence of counterparty risk, the steady marginalization of the dollar as the world’s reserve currency or, most likely, a combination thereof. Therefore, we view the upside potential to be as attractive as in 1999, before the 7.5x advance in the USD bullion price in the ensuing 12 years commenced.

We find that many investors who follow gold are on the sidelines, perhaps overly mindful of the poor performance of the past two years, and focused on market timing instead of the compelling long term picture. However, in the context of Western capital markets, such investors account for only a small sliver of the potential buying power. Gold and gold mining shares have never, in our opinion, been seriously considered as part of the mainstream conversation, which is in itself amazing in light of gold’s dramatic outperformance relative to all other assets from 1999 through 2011. Even after having been popularized by mainstream media as it was when making a significant top in 2011, gold was never perceived as anything more than a niche strategy. After two years of dispiriting performance, it is mired in investment purgatory.

There are two standout differences between now and 1999 in our view. First, a significant percentage of the above ground supply of physical gold has migrated from Western vaults to their counterparts in the Far East. Gold in that part of the world is viewed as a strategic asset, not as a trading vehicle, and therefore it is less likely to return to Western hands even if paper money valuations rise substantially. Much of the bullion that remains in the West, including central bank reserves, has in our opinion been encumbered by complex lending and leasing agreements, chains of rehypothecation, and other complex schemes concocted by bullion banks that would be extremely difficult to untangle on short notice. Competing or unclear claims to ownership in our opinion constitute the DNA of a potentially massive short squeeze. Second is the real possibility that the financial crisis of 2008 was not a one off event but rather the first manifestation of growing and unchecked systemic risk. Heroic post 2008 efforts by world central banks to stabilize economic activity may have only postponed a greater reckoning. Radical monetary policies implemented to restore order to capital markets may have become part of the problem by transforming bad private sector debt into sovereign credit while public policy generally failed to address underlying issues that led to the credit meltdown in the first place.

One does not need to subscribe to the possibility of extreme outcomes, however, to rationalize a commitment to gold right now. In our view, it is enough to say that it is deeply out of favor at a time when most other investment strategies remain popular. A contrarian view such as this would have served one well in 1999 before the dot com crash, the housing bubble, zero interest rates, toxic mortgages, 9/11, and the 2008 credit meltdown were in view. One can only speculate about future headlines, but the opportunity in gold, from a contrarian perspective is palpable and in our opinion, compelling.

Tocqueville Gold Strategy Monitor

With all best wishes,

John Hathaway

Portfolio Manager and Senior Managing Director

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

You are about to leave the site of Tocqueville Asset Management, L.P. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the any mutual fund managed by Tocqueville Asset Management, L.P. Please consider the investment objectives, risks, and charges and expenses of any mutual fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Poplar Forest (www.poplarforestfunds.com), by contacting an authorized broker/dealer, or by calling 1-877-522-8860. Please read the prospectus carefully before you invest. By accepting you will be leaving the site of Tocqueville Asset Management, L.P

You are about to leave the site of Tocqueville Asset Management, L.P. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the any mutual fund managed by Tocqueville Asset Management, L.P. Please consider the investment objectives, risks, and charges and expenses of any mutual fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Tocqueville Funds website (www.tocquevillefunds.com), by contacting an authorized broker/dealer, or by calling 1-800-697-3863. Please read the prospectus carefully before you invest. By accepting you will be leaving the site of Tocqueville Asset Management, L.P