Subscribe to Our Insights

Thought Leadership

Tocqueville Gold Strategy Investor Letter Third Quarter 2014

By John Hathaway on October 3, 2014

Through September 30, the $US gold price declined 6%, after giving up much of the stronger gains that had been achieved through most of the year. The recent bout of weakness began in late August and coincided with the breakdown of the Yen and the Euro vs. the US dollar. Commentary from all quarters is aggressively negative. Technical analysts are virtually unanimous in their bearishness. On a near term basis, this looks and feels like a bottom to us. On a longer term view, we are more bullish than ever.

Notwithstanding near term weakness in the gold price, most of our key holdings in the gold mining sector have managed decent gains, compared to a 2.78% decline for our XAU benchmark. We attribute our positive performance to our selection of well managed companies which are able to create value independently of gold price action. Value creation can come about in many ways, including accretive merger and acquisition activity, progress in the construction of new mines, or successful exploration. We continue to believe that investing in the securities of well managed gold mining companies offers the most dynamic and reliable exposure to the upside potential in the gold price. Our research activity and portfolio selection is based on emphasizing the value creators in the sector and avoiding the value destroyers.

The long term fundamentals for gold are stronger than ever, in our opinion. Overt currency debasement is the chosen path in Europe and Japan. The race to the bottom in these currency wars is not limited to our trading partners. In a recent article, Kenneth Austin, former chief economist for the Obama administration, calls for an end to US Dollar reserve status, seeing it as a drag on domestic growth. The use of the Chinese Renminbi to settle trades away from the dollar has grown dramatically in recent years. In the first half of 2014, the Bank of China cleared RMB payments equivalent to an impressive $18.3 trillion, double the previous year. The formation of institutions such as the new BRICs Bank and the Shanghai Gold Exchange enable participants to circumvent the $US and US financial institutions in the conduct of trade. The Chinese Central Bank has opened 1200 non-Chinese interbank clearing accounts to settle trades in Renminbi. In September, Britain announced plans to issue a Renminbi denominated bond. These are perfectly logical developments given the size of the Chinese economy and do not in and of themselves foreshadow a decline in the dollar. However, the advance of the Renminbi as a reserve currency does raise the question as to what central banks will do with a potentially huge surplus of dollars.

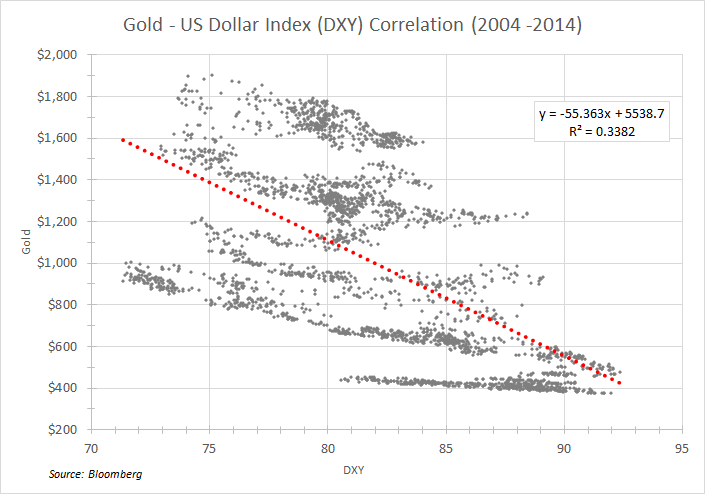

The US dollar strength that has been credited for the weakness in gold is in our opinion both an illusion and a misconception. The “strength” reflects only weakness of alternate reserve currencies and flight of speculative capital. We believe the condition to be of limited duration both long and short term. CFTC speculative trader dollar longs stand at a 15 year high, an extreme that typically marks an inflection point. The misconception is the notion that the dollar and gold trade inversely. The correlation coefficient between the dollar index and $US gold is only a weak .3389 since 12/31/03. The chart below demonstrates that the relationship between the gold price and the dollar index is quite tenuous.

The “strong” dollar, should it persist, will represent a dilemma for policy makers and politicians in the form of undesired deflationary pressures spanning the globe. For example, the weak yen threatens Chinese economic strength. Should that result in a round of currency debasement throughout Southeast Asia, the effect would be analogous to global monetary tightening via exchange rates, as suggested in a September note by Albert Edwards of SocGen.

Since the financial crisis of 2008, global leverage is greater than ever, both relative to GDP and in absolute terms. Global debt has increased 40% since 2008 versus a 22% increase in global GDP. The increased debt burden is manageable only because interest rates are at record lows. A rise in interest rates would in our opinion cause severe damage to financial assets, whose valuations have been inflated by money creation and zero rate of interest for risk free assets. Financial assets are valued based on discounted cash flows. In the ultra-low interest rate environment, what are the chances that the discount rate will decline from here? We suspect this could happen only if a collapse of expected earnings was foreseen. The prospect of higher rates would also create havoc, in our opinion, for credit quality. We believe that three things must happen to not upset the very unstable applecart in which financial asset values reside: 1) the pace of global growth must increase meaningfully; 2) debt issuance must stabilize; 3) inflation must remain tame. We also believe that the odds of achieving this trifecta are non-existent.

The just published 16th report on the global economy by The International Centre for Monetary and Banking Studies warns of “a poisonous combination of high and rising global debt and slowing nominal GDP….Contrary to widely held beliefs, the world has not yet begun to de-lever and the global debt to GDP ratio is still growing and breaking to new highs (160% in 2001; 200% in 2009; and 215% in 2013).”

Strong equity markets have been the major headwind for gold over the past three years, in our view. Who needs financial insurance when the weather is clear? Zero interest rates fostered by central bankers have forced money into risky and illiquid assets stretching valuations of lower quality categories to near record levels. Three years of positive returns have resulted in investor complacency.

Lofty financial asset valuations are not the only issue. What if fundamentals, economic growth and rising corporate earnings, begin to deteriorate? What if the Fed, intent on staying the course, begins to tighten into economic weakness? There are numerous examples of spreading economic weakness in the U.S. including recent soft data for housing, retail, and durable goods. Europe, already struggling, is facing increased headwinds from economic sanctions on Russia.

The gold/silver ratio has broken above a multiyear top of 68 and now stands at 71.3. As with credit spreads, this ratio is often a reliable signal of impending economic contraction. The behavior of this indicator is consistent with the persistent weakness of commodity prices. Credit spreads have begun to widen as well.

Expanding earnings and valuations, the underpinnings of the four year bull market in financial assets, may be approaching an inflection point. A reversal of this cycle would in our opinion restore interest in gold.

Sentiment indicators are at rock bottom levels. The Ned Davis Gold sentiment index has dropped to “0”, a level approached only once in the past eight years. Over the past 20 years, readings below 35 have reliably been followed by rallies. The Hulbert Gold Newsletter Sentiment Index currently stands at 46.9%, the second lowest reading in 30 years. These are cheery numbers to a contrarian, reminiscent of the low regard held for gold in the late 1990’s.

There is more than bleak sentiment going for gold. In our opinion, a gold supply crunch is around the corner. Headlines and front page stories on this are yet to come. Gold mining capital expenditures and exploration spending are in a virtual freeze mode. There have been almost no discoveries of large new gold ore bodies in the past 8 years. Ore grades are steadily declining and the world has become less hospitable in general to hard rock mining. We agree with Goldcorp CEO Chuck Jeannes’ prediction of peak gold production this year or next, to be followed by a multi-year decline. In our opinion, many producers are liquidating capital and reserves to tread water financially. We believe this will ultimately lead to a frenzy of takeovers, targeting both explorers and developers, the back bone of our portfolio. The Osisko takeover battle earlier this year exemplifies what we believe lies ahead.

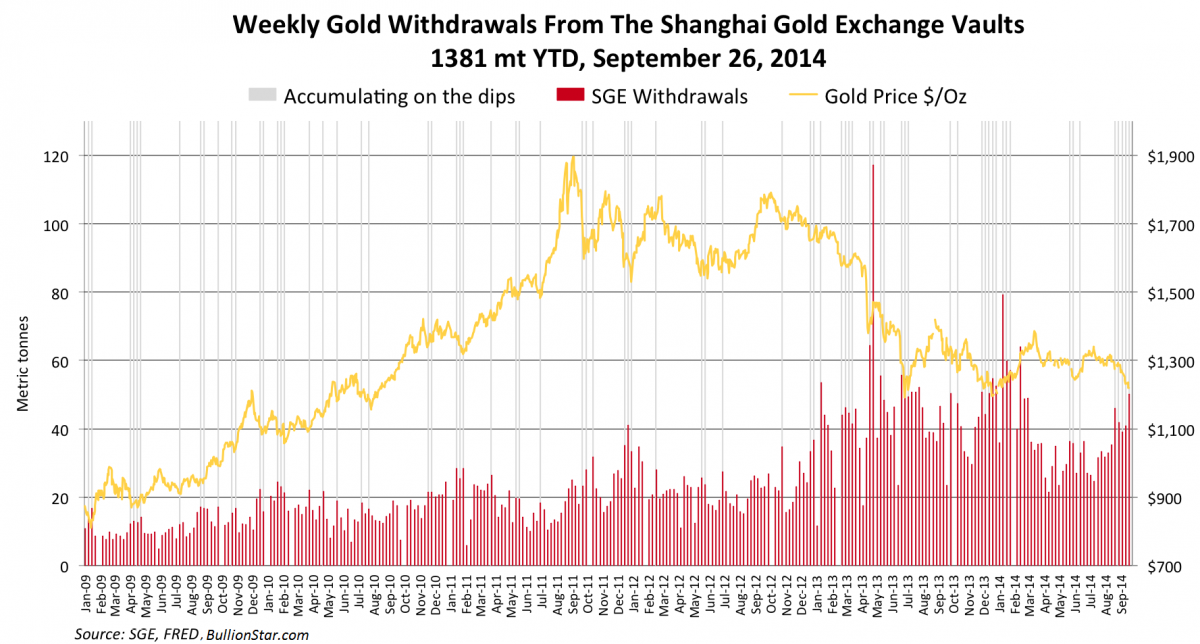

Another noteworthy development is the accelerated flow of gold bars from vaults in Western financial capitals to Asia and especially China. The magnitude of this shift can only be approximated and probably understated by official import statistics. A recent note by Na Liu of CnC China offers convincing arguments that 2013 Chinese demand was twice the 1000 tonnes reported by the World Gold Council and the China Gold Association, based on withdrawals from the Shanghai Gold Exchange. It must be noted, according to Mr. Liu, that none of the withdrawals from the SGE are accounted for by official sector demand. The puzzle of robust demand for physical gold accompanied by a declining gold price can in our opinion be understood only as a massive destocking by Western investors resulting in the transfer of bars from vaults in Western financial capitals to their counterparts in Asia. If Chinese consumption has been seriously underestimated as suggested here, the physical market is much tighter than conventionally believed. Therefore, only a modest reawakening of interest by Western investors could have an outsized impact to the upside.

The launch of the Shanghai Gold Exchange on September 18th is, in our opinion, emblematic of China’s intent to become a major force in the bullion market. In an editorial published July 30, 2014, Song Xin, President of the China Gold Association and Party secretary, stated that China should accumulate 8500 tonnes in official gold reserves, and that accumulation of the metal for official and private use was a matter of national interest. For reference, 8500 tonnes would require more than three years of global mine supply. Song’s predecessor had previously published an article in Quishi magazine (2012), the main academic journal of the Chinese Communist Party’s central committee which included the following passage:

The state will need to elevate gold to an equal strategic resource as oil. Currently, there are more and more people recognizing that “gold is useless” story contains too many lies. Gold now suffers from a “smokescreen” designed by the US, which stores 74% of official gold reserves, to put down other currencies and maintain the US Dollar hegemony. Going to the source, the rise of the US dollar and British pound and later the euro currency, from a single country currency to a global or regional currency was supported by their huge gold reserves.

Individual investment demand is an important component of China’s gold reserve system, we should encourage individual investment demand for gold. Practice shows that gold possession by citizens is an effective supplement to national reserves and is very important to national financial security.

This is a clear statement of China’s objective to elevate the Renminbi to reserve currency status, employing in part a strong backing of physical gold, if achieved, will dislodge the US dollar as a dominant reserve currency and in our opinion cause a significant re-pricing of the metal in US dollar terms. We do not believe that this outcome is what the bullish US dollar camp has in mind. The aggressive divestiture of gold by Western investors has been of immense assistance to Chinese ambitions. As suggested by Alan Greenspan in the latest issue of Foreign Affairs, the accumulation of a sizable gold reserve is a low risk, high reward path for China to offset the risk that their $4 trillion in foreign exchange reserves will be debased by their respective issuers.

We take comfort that our positive view of the future dollar gold price is shared by those who understand the difference between synthetic and physical metal, and who regard the real substance as a matter of strategic imperative, not as plaything for macro traders. We believe that China’s negative assessment of the future prospects for the US dollar is correct and that our investment strategy of investing in the shares of value creating gold miners offers sensible and dynamic exposure to the inevitable re pricing of gold in US dollars.

Tocqueville Gold Strategy Monitor

With all best wishes,

John Hathaway

Portfolio Manager and Senior Managing Director

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

View PDFPoplar Forest

You are about to leave the site of Tocqueville Asset Management, L.P. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the any mutual fund managed by Tocqueville Asset Management, L.P. Please consider the investment objectives, risks, and charges and expenses of any mutual fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Poplar Forest (www.poplarforestfunds.com), by contacting an authorized broker/dealer, or by calling 1-877-522-8860. Please read the prospectus carefully before you invest. By accepting you will be leaving the site of Tocqueville Asset Management, L.P.

Tocqueville Funds

You are about to leave the site of Tocqueville Asset Management, L.P. The link you have accessed is provided for informational purposes only and should not be considered a solicitation to become a shareholder of or invest in the any mutual fund managed by Tocqueville Asset Management, L.P. Please consider the investment objectives, risks, and charges and expenses of any mutual fund carefully before investing. The prospectus contains this and other information about the Funds. You may obtain a free prospectus by downloading a copy from the Tocqueville Funds website (www.tocquevillefunds.com), by contacting an authorized broker/dealer, or by calling 1-800-697-3863. Please read the prospectus carefully before you invest. By accepting you will be leaving the site of Tocqueville Asset Management, L.P.